Litmus test for Dr. LAL PATHLABS

Innovation distinguishes between a leader and a follower.

Steve Jobs

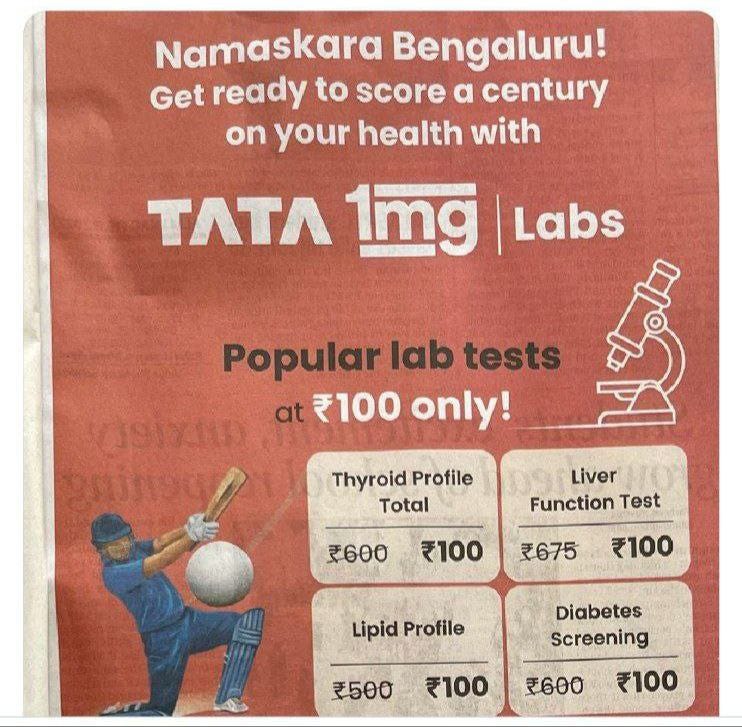

Lets come to a point, where we get to talk about the title “Litmus test for Dr LAL PATHLABS” . Few days back TATA 1MG came with an advertisement,

in which they were offering a range of diagnostic tests for just Rs 100 each as against around Rs 600, that many others in the industry charge at the moment. This advertisment was solely able to shook the diagnostic industry, then came a tweet from Mr. Velumani , the founder of Thyrocare, a leading and listed diagnostic major. The tweet has unleashed a wave of renewed discussion within the Indian diagnostic industry on where it is headed.

During this discussion the stock prices of major listed diagnostic companies have taken a huge hit. Likes of DR LAL PATHLABS, METROPOLIS and THYROCARE were crushed like there is no tomorrow. No wonder this Tata 1MG advertisement has created a havoc inside diagnostic industry. Specially for DR LAL PATHLABS, as the leader was bleeding the most.

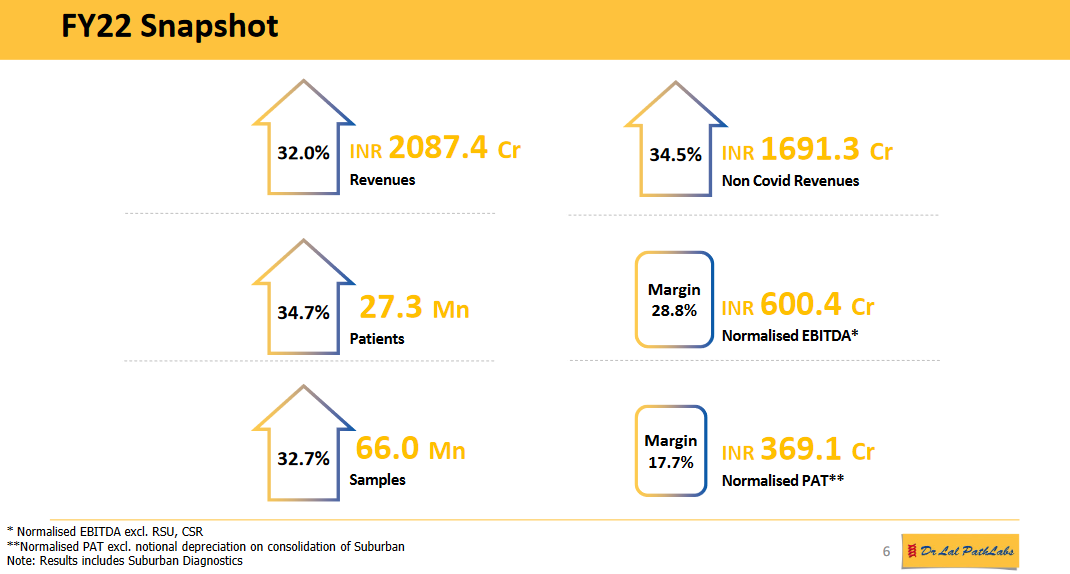

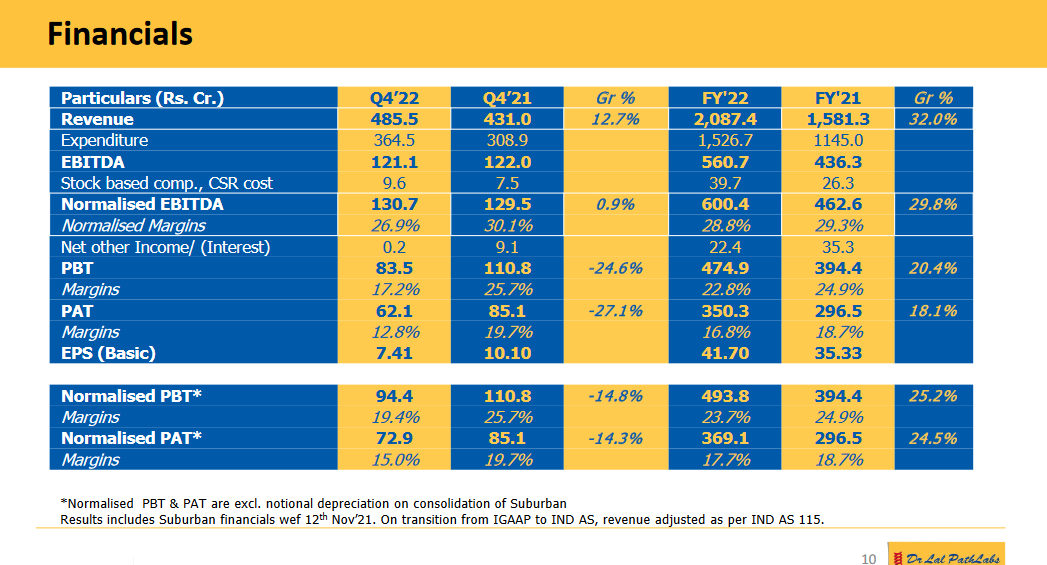

Few days after the advertisment, there comes the more pain for shareholders of the company. The results were out and it missed all the estimates. Excluding Suburban, DLPL’s non-Covid sales growth disappointed at just 4.3% yoy (-5.6% qoq). It did manage to replenish there numbers YoY, but disappointed QoQ.

Commenting on the results announcement, (Hony) Brig. Dr. Arvind Lal, Executive Chairman said: India remains a largely underserved market for diagnostics. The scope for growth for companies like ours is huge and we want to leverage our position as a leading player. At Dr. Lal PathLabs, we see ourselves as a progressive

brand and have been at the forefront of integrating technology into our business model. This helps us reduce costs as well as provide a more seamless and cohesive experience to our patients. We continue to invest in latest technologies across medical science and patient service in line with out vision of being the most trusted healthcare partner.

On being asked about the competition and there pricing schemes, management told that competition is more visible now versus earlier. Some of these

pricing actions by competitors are promotional strategies in select cities. Management told that, brand building in healthcare is more complex than other consumer-focused sectors. For now, DR LAL PATHLABS does not want to follow competitors and lower its pricing but also mentioned that ‘time will tell’. DLPL agrees that prolonged increased competition will have an impact on its business.

If we talk about the stock price of DR LAL PATHLABS, then it is nothing less than a carnage for the shareholders. Stock has corrected more than 55% from its Peak.

Trading at PE of 47, EV/EBITDA of 26 and BV of 10.85 which is still higher than its peers. Although DR LAL PATHLABS is a huge FCF generating business and as a market leader these valuations can be justified after the recent corrections.

As an Investor one should keep everything check and analyse where this industry is going on and How this competition is going to play out. The microeconomics is very much not same for diagnostic industry, but this is the beauty of innovators and Disruptors. This is going to be a watchful Litmus test. Is competition going to survive or the existing leader will emerge as an undisputed winner.

Like, share and subscribe if this post has added some value to your Investing journey.

Disclaimer- Please do your own Due diligence, before buying or selling.

Thankyou